Overview

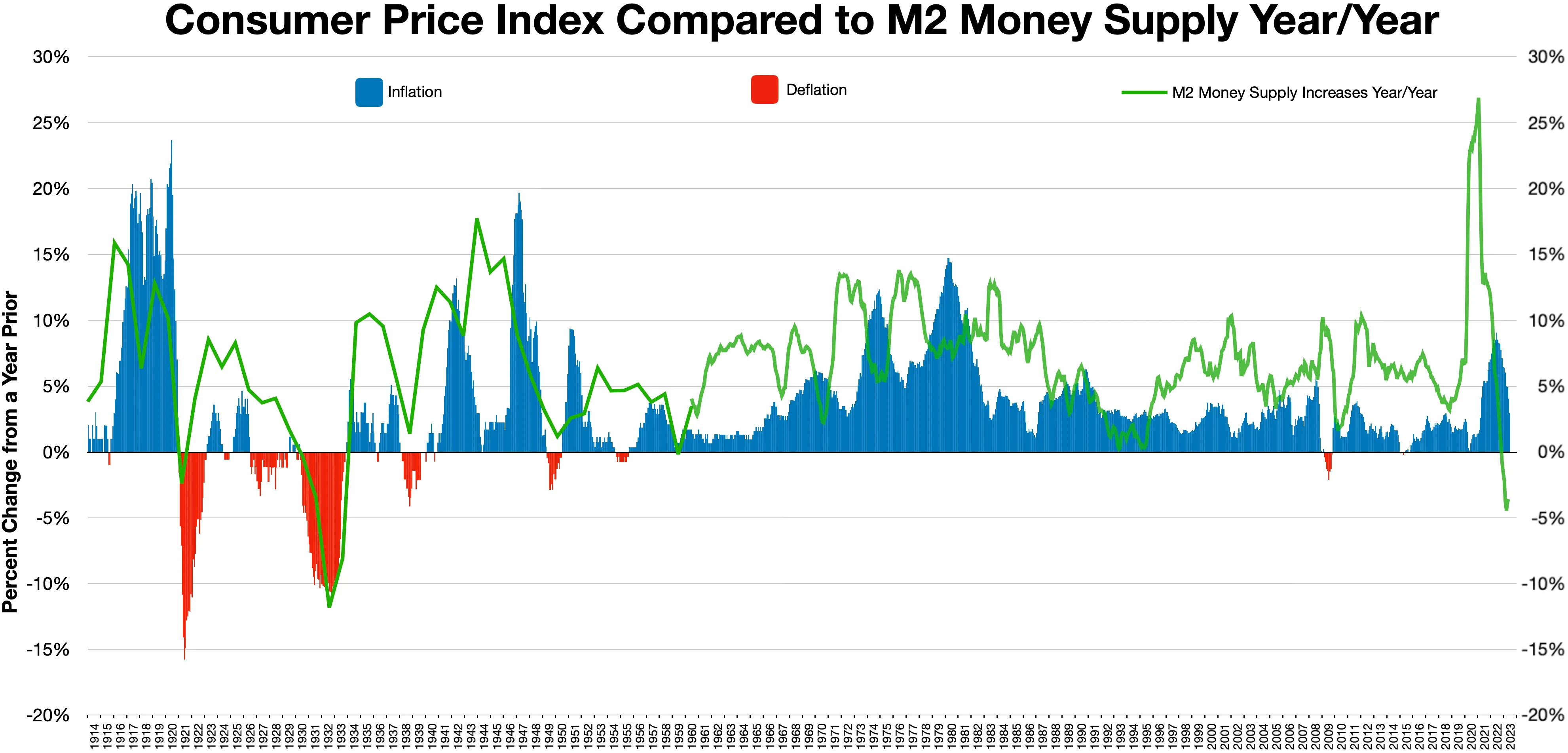

Monetarism places the quantity of money at the center of macroeconomic analysis, contending that changes in the money stock have predictable effects on output, employment, and especially the price level. Its most famous formulation, the quantity theory of money, is expressed by the equation MV = PY (money supply × velocity = price level × real output). Monetarists argue that, in the short run, velocity is relatively stable, so systematic changes in M translate directly into proportional movements in P (inflation) when the economy operates near full capacity. Consequently, they advocate for a rule‑based monetary policy—most famously a constant growth rate of the money supply—to avoid the discretionary, politically driven interventions that can generate “inflationary spirals.”The school emerged as a reaction to the Keynesian consensus that emphasized fiscal policy and demand management. Monetarists warned that excessive reliance on fiscal stimulus and activist monetary easing could erode the credibility of central banks, leading to unanchored inflation expectations. By the late 1970s, their message resonated with policymakers confronting stagflation—a combination of high inflation and stagnant growth that traditional Keynesian tools struggled to resolve.

History/Background

The intellectual roots of monetarism trace back to classical economists such as David Hume and Irving Fisher, but the modern incarnation crystallized in the 1950s and 1960s through the work of Milton Friedman and his Chicago School colleagues. Friedman’s 1956 paper “The Role of Monetary Policy” and his 1968 book A Monetary History of the United States, 1867‑1960 (co‑authored with Anna Schwartz) provided empirical evidence that the Great Depression was deepened by a sharp contraction in the money supply. These publications shifted the academic debate toward a greater focus on monetary aggregates.Monetarism gained political traction during the early 1970s, when the United Kingdom’s Labour government under Harold Wilson appointed Sir Geoffrey Howe as Chancellor, who experimented with targeting monetary aggregates. In the United States, Paul Volcker, appointed Federal Reserve Chairman in 1979, adopted a policy of aggressively tightening money growth to break the back of double‑digit inflation—a move widely credited to monetarist logic, even though Volcker ultimately relied on interest‑rate adjustments rather than strict money‑supply targets.

By the mid‑1980s, the original monetarist prescription of fixed money‑growth rules fell out of favor. Empirical research revealed that the velocity of money was far less stable than assumed, especially amid financial innovation and deregulation. Central banks shifted toward inflation targeting, using the policy interest rate as the primary instrument, a framework that retained the monetarist emphasis on price stability but abandoned direct control of monetary aggregates.